Brilliance China (1114 HK)- Asymmetrical bet with 80-110% upside in two months!

Dear readers,

This is my first memo on Substack. I feel mostly grateful to have you as my readers. Please allow me to have a brief intro of myself first. I’m from China. I consider myself a value investor (not that ‘value’ actually, as I have walked through the way from Graham to Buffett and focus more on compounders). Three years ago I went to Columbia University for the Value Investing Program. After graduation, I decided to go back to my homeland to catch the ‘compelling long-term growth of China’. Unfortunately, the plan crashed (check out the political news in China of last weekend, or simply this Monday’s stock performance of Chinese ADRs). So I got another plan- to fish in other ponds, where laws and rules count and the analysis frameworks I learnt from school can be applied.

Recently I signed up with some really good newsletters on Substack and followed some good investors bloggers on Twitter. Their wisdom and generosity enlightened me a lot. So I made the decision to start my own, in the hope to give back to the value investing community and to make more friends. My plan is to share my memo mostly on non-Chinese stocks, yet my apologies for starting with a Chinese one. This one just looks too attractive- it's a special situation and has a different risk profile with other opportunities (Chinese or non-Chinese, economic or political uncertainties. As a long-term and fundamental-driven investor, I suffered a lot this year :( ).

Without further ado, let’s go to the point- China Brilliance (1114 HK). The company does not have much business under its operation, apart from an auto components manufacturing business and an auto financing business, generating c600 mm HKD revenue in 22H1. But it has a lot of assets.

In a nutshell, it has 19 bn HKD as net cash (all liabilities deducted), 25% stake in the BMW China JV1 (which earned 31 bn HKD as net income in 2021. So 8 bn HKD belonged to China Brilliance), plus the BMW China JV has 43bn HKD net cash. Those amount to 50-55 bn HKD as net assets, if we value the BMW stake at 3x PE.

Yet the market cap by Oct 25th, 2022 was 16.8 bn HKD!

Everybody hates Brilliance China

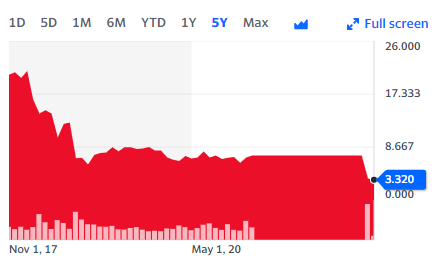

You must wonder why it is so undervalued. Simple. The corporate governance is crap. Check out the price chart and you know the company and management are loser of the losers:

Chart: Brilliance China’s stock 5-year price chart by Oct 25th, 2022

Source: Yahoo Finance

It’s a state-owned company, even a very bad one among its state-owned peers.

Their German partner cursed them.

The proceeds from the sale of the 25% BMW JV stake was 27.9 bn RMB. Ironically, they were taxed with 7.3bn RMB, while the gain was only 4.9bn. What a rate! Plus, considering BMW China only paid out 20% of the 2019-2021 earnings as dividends, the deal price was actually 17bn HKD, or 2.3x 2021 PE.

All its other ventures have been proved failures.

In March 2021, the auditor found the management of a subsidiary provided 7.5bn-HKD-guarrantee for its controlling shareholder Brilliance Auto, which has been under Chapter 11 since Oct 20202, without the consent of the Board. So the shares of the company on the HK Stock Exchange has been suspended since then.

Even after all the mess, the company only replaced 4 of its 8 Board members. I’m surprised Chairman Wu still remains on the Board, as he was and is the Chairman of the subsidiary which provided guarantee for Brilliance Auto.

The stock resumed trading from Oct 5th, 2022. When I told an American friend of mine about the opportunity, he shared that it was the company’s 2018 BMW JV deal destroyed all his confidence in Chinese state-owned companies and he hates them out of his guts. People just stay away from it.

What’s the catalyst

So you understand why it’s undervalued. Could it be a value trap? If just for the cash sits on its and BMW JV’s bank account, I’d say probably. I’ve seen too many Chinese companies with tons of cash piled up on their balance sheet but never distributing a penny to shareholders, so usually I don’t deduct the cash when I calculate the value of those companies (in fact, I tend to stay away from these kind of stocks). The good thing is, they are planning to pay it out.

Then the question comes to- how much? I don’t have an clear answer, but I’m confident it would not be zero, and could be a lot.

In its 2019 annual results conference, one investor asked the Chairman Mr. Wu if the company would pay special dividend once the 25% BMW transaction is closed. Mr. Wu said ‘we have always promised this’.3

In its Aug 22, 2022 announcement, the company said ‘the company has always been considering to use the proceeds from the sale of BMW JV to create value for shareholders. Potential measures include three, but not limited to three, options: special dividend, share repurchase, or reinvestment.’

In a recent sell-side notes, the newly appointed CFO said ‘the Board would make the decision by the end of 2022 on how to distribute the cash. By mid Oct, we don’t have any reinvestment opportunities at hand. So I believe the Board would distribute the cash (without mentioning how much) to shareholders. Many shareholders hope we could do it quickly. The Board acknowledge it and agree to move forward ASAP.’

The CFO also mentioned ‘the BMW JV has a lot of cash and cashflow, so it does not need reinvestment. We have written off the loss-making Renault JV and Jinbei businesses, so we won’t reinvest in them. Other subsidiaries such as auto finance and auto parts are very mature, so I don’t see they need any reinvestment.’

It looks certain to me the company would pay special dividend. Given the company is trading below net cash and at 2-3x PE, I don’t think the market is vesting a big pay-out ratio, if there is any. Citi’s most recent report assumed a 25-50% payout and gave it a buy-rating with TP of 7.1 HKD. So the upside from this bet is any amount it would pay out.

Why would the company want to pay them out? It’s complicated as there are multiple stakeholders, starting from

Public shareholders are more than willing to pay all the cash out. How I wish they could sell the remaining 25% BMW stake and pay it out too! By Jun 30th ,2022, Baillie Gifford held 9.98% of the company. I’m very curious about their plan.

The management looks kind of irrelevant to the issue. The management of SOEs are more of government officers and they obey the order from the higher-level officers. Apart from the Chairman Wu, no one on the board or C-suit hold any stakes in the company. Even the Chairman’s holding only worth 2-year equivalent of his annual income. The incentive doesn’t look big enough. But they have made the pledge anyway. Could they have relatives and friends buy the stock for them? I don’t rule out the possibility. Since the stock resumed trading in Oct, the company only met selective investors. I reached out to the company and they said they would only start to meet investors after the AGM on Nov 11th. Could it be their proxies are collecting stock for them during this window? It’s possible.

The largest shareholder Brilliance Auto, who holds 30.43% of the holdings, is under Chapter 11. I don’t think this question matters to them anymore.

But how about Brilliance Auto’s creditors? On the bright side, the more Brilliance Auto got from China Brilliance as dividend, the better. On the dark side, they could somehow lower the paper-value of the 30.43% stake to get a bigger share of the assets, and then realize the value through capital allocation. Yet I think it’s not easy as there are c300 creditors and nobody has a decisive share. Do the creditors of Brilliance Auto has a say on the dividend decision of China Brilliance? Honestly I’m not sure. Yet clearly the Board of China Brilliance don’t think it’s a problem.

The second largest shareholder Liaoning Jiaotong Investment, who is a SOE and controlled by the Liaoning provincial government (same as Brilliance Auto), has two options: either to agree on the pay-out and take the cash, or negate it so they can use/steal the all the cash as they did in the past. It’s hard to say as I believe there are multiple stakeholders behind the scene. Yet since the company has announced the distribution, I believe they are good with it.

Based on the analysis, I believe paying out special dividend is the option that benefits everyone. It’s better than share repurchase as the creditors of Brilliance Auto and Liaoning Jiaotong are better off to have the cash than a higher stock price.

What are the other risks of the dividend? The one I can think of is whether the ForEx Administration of China allows the company to exchange 10+ bn RMB into HKD, as China has been tightening forex outflow for years. Maybe the management would give a clearer explanation in the Nov 11th AGM.

How much the remaining businesses worth?

BMW China

America is a country built on wheels. Yet Chinese people love cars more, not the mobility per se, but the nobility endorsed by the brand. Benz, BMW and Audi are the three dominators of luxury cars with the price range between 70k-100k USD. BMW ranked No.1 in terms of sales volume among all the luxury brands in China, with 20.8% market share in 2021. The JV is super profitable that its 2021 adj. ROE exceeded 70%. Even though BMW’s lower end models are facing competition from Tesla and other domestic NEV brands, as well as pressure from the slowing Chinese economy, it’s fairly safe to assume the JV to earn 20-25bn HKD each year in the short- to mid-term future.

Source: China Brilliance company filings

Note: 1. the figures are converted to HKD at current 0.925 RMB/HKD rate, not historical 2. Adj Equity = Equity - (Cash and equivalents - Current & non-current debts)

The next question would be whether the JV’s 43bn HKD net cash would be paid out. Obviously BMW China has retained too much cash in 2020 and 2021. On this subject, China Brilliance’s CFO commented:

‘The JV did not pay dividend because China Brilliance was under investigation in the past 18 months. Large sum of pay-out would complicate the process.’

‘The JV does not need that much of cash.’

‘If we got the cash dividend from the JV, we would consider distribute to shareholders as dividends.’

Upon the 25% stake sale agreement in 2018, BMW made a soft guideline to pay out 30% of the JV’s net profit each year. The CFO said the future pay out ratio would be upon the consensus of BMW and China Brilliance. In my opinion, China Brilliance’s cash flow would be fully dependent on the JV’s dividend. So the company does have a strong incentive to require dividend.

How much does the earnings power of the 25% stake worth? I think it’s anywhere between 15bn and 30bn HKD:

Assume the JV pays out 1.5bn HKD (tax deducted) as dividend, the business worth 15bn HKD under a 10% discount rate.

Assume the JV can earn 25bn HKD this year and we assign 3x PE to it, it’ll be 19bn HKD.

The book value of the 25% stake is 11.8bn HKD, excessive cash excluded. But remember it’s a 70% ROE business.

The deal price for the other 25% was 30bn HKD.

I prefer 20bn HKD. The key is it’s higher than the current market cap.

Other businesses

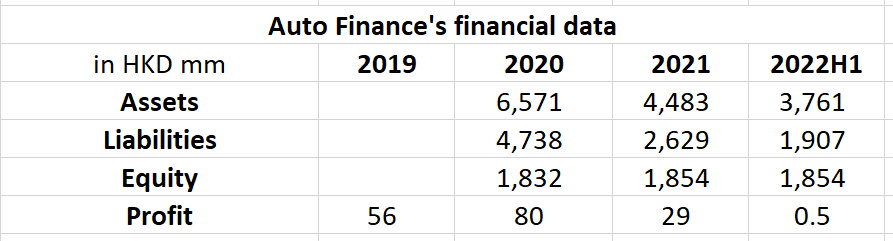

The auto finance is a solid business. Safe balance sheet and profitable. The company has been scaling down the business.

Source: China Brilliance company filings

Note: the figures are converted to HKD at current 0.925 RMB/HKD rate, not historical

The non-BMW manufacturing business is a money shredder. The silver lining is the company is scaling them down. The Renault JV was written down in Jan 2022. The liabilities decreased from 7,554mm HKD to 1,094mm HKD in 22H1, which is very reassuring. However, it still booked a 431mm HKD loss in 22H1, which is difficult to understand.

From the sell-side notes, the CFO suggested the 431mm loss was mostly write-downs. He also said ‘in the past 18 months, we made some reorganization of the business, shutting down loss-making or unpromising subsidiaries. Up to today, 80-90%, or nearly 100% of the remaining businesses are profitable. I don’t think they’ll bring losses if things are normal (no severe COVID lockdown).’

Source: China Brilliance company filings

Note: the figures are converted to HKD at current 0.925 RMB/HKD rate, not historical

The company also incurred tens of millions HKD central costs every year. It is well beyond me what have cost so much for a shell company. Well, I’ll just assume the costs would be 100mm HKD a year going forward.

Source: China Brilliance company filings

Note: the figures are converted to HKD at current 0.925 RMB/HKD rate, not historical

Any more surprises?

For safety, I assume all those other businesses and central costs would incur a 1bn HKD loss every year. Would there be any more ‘earnings surprises’, or any more skeleton in the closet? I believe the chances are slim, as the incident has been fermented for 18 months, long enough to let the problem emerge. Quote the CFO:

‘An independent agency, RSM, has done two rounds of investigations, on every bank log.’

‘It’s been 18 months, if there are more guarantees or alike, the creditors would sue.’

‘An auditor, Dahua, has checked the internal control on every subsidiaries, except for those are going to be liquidated.’

‘Dahua provided a report after the internal control investigation. We have handed the report over to regulators. That was why we were allowed to resume trading.’

‘We have hired a specialist to monitor related transactions.’

‘We will require those management members who serve in both China Brilliance and Brilliance Auto to resign from either party.’

Conclusion

Given the strong position of BMW in China and China Brilliance has written down and closed most of its unprofitable businesses, the downside risk for China Brilliance stock would be limited at 3.3HKD a share.

We can assume China Brilliance gets 6.75bn HKD from BMW JV every year, and the other businesses cost 1bn HKD each year. Put a 3x PE to the net earnings, it’s c 16bn HKD, or 3.12 HKD per share.

The 11bn HKD on BMW JV’s bank account could be extra upside, I give it a 40% discount so it worth 1.28HKD per share.

The upside is the special dividend from the 19bn HKD net cash. We would know the payout ratio in two months. And more people would notice it after the AGM on Nov 11th.

I suspect the company would pay out 50-80% of the 19bn HKD cash as dividends, with a 15% tax, so share holders can get from 8bn to 13bn HKD, or from 1.6 HKD to 2.56 HKD per share.

In my opinion, the more the management pays out, the higher multiple its operating profit would get. Because the market would put a lower holding discount to its 25% stake in BMW China, if they do smart job on capital allocation.

In my opinion, the right strategy for this bet is to sell on the day when the payout ratio is announced. Given the poor track record of the company and very uncertain outlook of China, it’s unwise to hold it for a long time, or a very large position in the portfolio. The exception is if the payout ratio is really high but the market does not respond at once, it’s better to wait for a day or two for the market to absorb.

Disclaimer

This article is solely for informational purpose and not an investment advice. Please do your due diligence work. The information in the memo are based on public information and my own opinion, which could be inaccurate and wrong.

I personally own China Brilliance (1114 HK) stock.

PS

Really appreciate your time and patience. You are more than welcome to share this memo with your firends, subscribe for my Substack channel, or follow me on Twitter with @SnowsofNebraska (I still had NONE followers by the time I wrote this memo. Please!). I’ll share my research on other interesting investments in the future. If you are interested in the idea or have any thoughts, you can leave a comment or reach me with zf2221@columbia.edu. Many thanks!

China Brilliance owned 50% stake of the JV before it sold 25% in Feb 2022. Previously the Chinese government requires that foreign auto manufactures must have a JV partner in order to produce cars in China, and the ownership of the foreign partner could not exceed 50%. In 2018, Chinese authority released that requirement and foreign ICE vehicle manufacturers are allowed to own more than 50% starting from 2022. In Oct 2018, China Brilliance announced it would sell its 25% stake to the German partner in 2022 for RMB 290 bn (or roughly 320 bn HKD). FYI, China Brilliance’s market cap was 100 bn HKD in early 2018, meaning the market thought the value of the 25% stake was well above 50bn.

https://finance.sina.com.cn/stock/s/2022-07-24/doc-imizirav5218921.shtml

https://www.zhitongcaijing.com/content/detail/191946.html

Great write-up, Alex. What are your preferred sources to follow news, management comments, et cetera of Chinese/HK businesses?

Opps Jinbei spending more money it seems